Crypto

How Russia Benefits from the Power of Cryptocurrency in 2025

Introduction

As the global financial landscape continues to shift, Russia has embraced cryptocurrency as a strategic tool to bypass economic challenges and gain a competitive edge. In 2025, crypto is no longer just a digital asset in Russia — it’s a cornerstone of its evolving economic policy. From international trade to fintech innovation, Russia is tapping into the power of crypto to rewrite the rules of global finance.

How Russia is Using Cryptocurrency to Bypass Sanctions

One of the most significant ways Russia benefits from cryptocurrency is through its ability to evade international sanctions. With traditional banking channels restricted, the Kremlin and Russian businesses are increasingly relying on decentralized finance (DeFi) and digital currencies to conduct international transactions.

Key Points:

- Russia is using Bitcoin, Ethereum, and stablecoins to settle cross-border payments.

- Crypto wallets allow discreet financial movements beyond the control of Western banks.

- Blockchain-based systems are helping Russia build alternative financial routes with countries like China, Iran, and India.

Strengthening Economic Independence

Russia views crypto as a shield against Western financial influence. By encouraging the use of digital ruble (CBDC) and supporting private crypto initiatives, the government aims to create a parallel digital economy that reduces reliance on the U.S. dollar and SWIFT.

Strategic Benefits:

- Digital Ruble pilot programs rolled out in key regions.

- Increased support for crypto mining operations in energy-rich areas like Siberia.

- Rising domestic adoption of blockchain technology in logistics, banking, and real estate.

Boosting Innovation and Tech Development

Cryptocurrency is also driving technological innovation in Russia, especially in sectors like fintech, cybersecurity, and smart contracts. The country is investing in blockchain-based infrastructure to foster homegrown tech startups and attract foreign crypto investors.

Highlights:

- Government-backed incubators for crypto and blockchain startups.

- Partnership with BRICS countries to launch blockchain-based payment systems.

- Academic and corporate collaboration to develop Web3 applications.

Russia’s Growing Role in the Global Crypto Economy

Despite geopolitical isolation, Russia is becoming a significant player in the global crypto space. It ranks among the top countries for crypto mining, crypto wallet usage, and blockchain development. The country’s natural gas and oil reserves also provide cheap energy — a critical asset for mining operations.

Ranking Stats (as of 2025):

- Top 5 in global Bitcoin mining.

- Over 10 million active crypto users in Russia.

- Leading contributor to open-source blockchain projects in Eurasia.

Challenges and Risks

While the benefits are clear, Russia’s crypto strategy also faces challenges:

- Regulatory uncertainty in international crypto markets.

- Risk of cybercrime and money laundering.

- Potential backlash from global watchdogs like FATF and IMF.

Conclusion

In 2025, Russia is strategically leveraging cryptocurrency to assert its financial independence, boost economic innovation, and outmaneuver global constraints. Whether viewed as a survival tactic or a long-term pivot, Russia’s embrace of crypto is reshaping its place in the global economic order.

Discover more from The CoinStar

Subscribe to get the latest posts sent to your email.

Business

MARA’s $1.1 Billion Bitcoin Sale Isn’t a Retreat—It’s a Strategic Pivot to Dominate AI Infrastructure

For the better part of two years, the market narrative surrounding publicly traded Bitcoin miners has been caught in a binary tug-of-war. On one side, they are pure-play proxies for the price of Bitcoin. On the other, they are energy infrastructure companies masquerading as crypto businesses.

On March 26, 2026, MARA Holdings (NASDAQ: MARA) delivered a masterclass in how to reconcile these two identities, sending shares up more than 10% in pre-market trading after announcing a surgical restructuring of its balance sheet that signals the end of the “hodl-at-all-costs” era and the beginning of a new playbook for digital asset compute .

The headline numbers are striking, but the strategic nuance is where the story lies. MARA sold 15,133 Bitcoin between March 4 and March 25, netting approximately $1.1 billion. This wasn’t a fire sale born of desperation; it was a calculated deployment of capital to repurchase roughly $1 billion of its 0.00% convertible senior notes due 2030 and 2031 . By buying back the debt at a roughly 9% discount, the company captured $88.1 million in immediate value and slashed its convertible debt load by 30%—from $3.3 billion to $2.3 billion .

In a single move, MARA reduced future shareholder dilution, strengthened its balance sheet for an aggressive expansion into AI and high-performance computing (HPC), and proved that its massive Bitcoin treasury is not just a speculative asset, but a strategic war chest.

The Art of the Debt Deal: Why 0% Notes Matter

To understand why the market rewarded this news with a double-digit pop, one must first appreciate the peculiar nature of the liabilities MARA just retired. The company issued 0.00% convertible senior notes—instruments that pay no interest but carry significant potential dilution risk. If MARA’s stock price appreciates above the conversion price, note holders convert debt into equity, diluting existing shareholders .

When a company like MARA repurchases these notes at a 9% discount to par value, it effectively buys back future equity at a discount today. It is a capital allocation strategy typically reserved for mature technology firms with predictable cash flows, not volatile crypto miners. CEO Fred Thiel framed the transactions as a preservation of shareholder value, stating that the move was designed to “strengthen our balance sheet and position the company for long-term growth” .

This is a distinct departure from the industry’s historical tendency to hoard Bitcoin regardless of market conditions. By utilizing its holdings to deleverage, MARA is signaling a maturation of the sector—one where balance sheet health and strategic optionality outweigh the vanity metrics of treasury size.

The AI Bottleneck Is Power: The Starwood Partnership

The most critical line in the company’s announcement is buried in the section labeled “General Corporate Purposes.” While the debt buyback is the immediate catalyst for the stock movement, the reason for cleaning up the balance sheet is the far more compelling long-term thesis: the convergence of Bitcoin mining infrastructure with artificial intelligence.

Earlier this year, MARA announced a strategic partnership with Starwood Capital Group, a global investment firm managing over $125 billion in assets . The deal is not simply a lease agreement; it is a joint venture to convert existing MARA mining sites into high-performance computing data centers capable of hosting AI workloads.

Here is why this is savvy. The primary bottleneck for AI expansion in 2026 is no longer just semiconductor chips—it is power. Building new hyperscale data centers from scratch requires navigating a permitting and grid-connection process that can take seven to ten years . MARA, however, already sits on energized land. The company’s Bitcoin mining portfolio spans multiple states with pre-existing, industrial-grade power infrastructure.

Under the Starwood partnership, Starwood Digital Ventures (SDV) will handle design, tenant sourcing, and construction, while MARA contributes the power-rich sites. The initial phase targets 1 gigawatt (GW) of IT capacity, with a roadmap to scale beyond 2.5 GW .

The genius of the model is that mining serves as the flexible foundation. As Thiel’s team has outlined, mining is a “flexible workload” that generates revenue immediately. If a site is slated for AI conversion, mining continues to operate until a tenant is ready. If AI demand dips, the capacity reverts to mining. This creates a floor on asset utilization that pure-play AI data center developers lack .

Peers in the Rearview: How MARA’s Strategy Differs

To appreciate the discipline of MARA’s approach, one must look at the broader landscape of Bitcoin miners pivoting to AI. The sector has seen a flood of announcements, but the execution strategies vary widely, often leading to market bifurcation.

- Core Scientific (CORZ) and TeraWulf (WULF) have been the pioneers of the AI pivot, successfully signing massive HPC hosting contracts. Core Scientific, for instance, saw colocation revenue nearly quadruple year-over-year, though it came alongside a significant liquidation of Bitcoin holdings . TeraWulf, arguably the most aggressive in the pivot, signed over $12.8 billion in long-term contracts but ended 2025 with a mere 3 BTC on its balance sheet, effectively exiting the treasury game entirely to fund the transition .

- Iris Energy (IREN) has taken perhaps the purest approach, liquidating Bitcoin daily to fund GPU purchases, holding no strategic treasury .

- Riot Platforms (RIOT) and CleanSpark (CLSK) have remained more focused on pure-play mining, though Riot has also signaled a pivot toward HPC, reporting a massive loss recently as it invests heavily in infrastructure .

MARA sits in the sweet spot between these extremes. Unlike TeraWulf, MARA retains a substantial treasury—38,689 BTC valued at roughly $2.7 billion . Unlike IREN, it is not selling every coin it mines. And unlike some peers racing to sign HPC leases that may or may not be profitable given current power costs, MARA is leveraging a partnership with Starwood to de-risk the development cycle .

This disciplined approach has not gone unnoticed. Analysts have noted that while the industry’s shift to AI creates a short-term supply overhang (as miners sell BTC to fund capex), it ultimately strengthens the long-term health of the network by reducing uneconomic hashrate . MARA’s move is the most sophisticated execution of this thesis to date.

The Macro Implications: A New Treasury Strategy

The decision to sell such a significant chunk of its Bitcoin holdings marks a philosophical shift for the industry. For years, the “Strategy playbook”—hoarding Bitcoin and issuing debt to buy more—dominated corporate treasury strategies among miners. But in 2026, the calculus has changed.

Bitcoin mining economics are under pressure. The network hashrate remains high, and the halving cycle has squeezed margins. In such an environment, holding a massive, non-yielding asset on the balance sheet while carrying billions in convertible debt is a luxury few miners can afford when faced with the capital-intensive demands of AI infrastructure.

By converting a portion of its Bitcoin into debt reduction, MARA is effectively swapping volatility for stability. The reduction in outstanding convertible notes reduces the risk of massive share dilution in the future, which is a primary concern for institutional investors. It also frees up the balance sheet to pursue the Starwood venture without needing to issue more dilutive equity or tap debt markets at potentially unfavorable rates.

Risks and the Road Ahead

It would be irresponsible to suggest this is a risk-free maneuver. The sale of Bitcoin reduces MARA’s exposure to a potential upside rally in the crypto market. If Bitcoin were to enter a parabolic phase later in 2026, MARA would benefit less than its more “hodl”-focused peers.

Furthermore, the pivot to AI/HPC is not a guaranteed victory. The market for AI compute is competitive, and hyperscalers like Amazon, Microsoft, and Google have deep pockets. While MARA has power, it is entering a market where customer relationships and operational expertise in cooling high-density GPU clusters are paramount. The success of the Starwood joint venture hinges on signing anchor tenants for that 1 GW of capacity—a process that is currently underway but not yet finalized .

There is also the matter of the remaining debt. While MARA reduced its convertible notes by 30%, it still carries roughly $2.3 billion in such instruments . The company also holds $632.5 million of the 2030 notes and $291.6 million of the 2031 notes that remain outstanding, alongside other maturities . The balance sheet is healthier, but not pristine.

Conclusion: A Blueprint for the Next Generation of Miners

As the trading day unfolds, the 10% surge in MARA’s stock price suggests that investors are not treating this Bitcoin sale as a capitulation, but as a strategic upgrade. Fred Thiel and his team have articulated a vision where MARA is not just a Bitcoin miner, but a diversified digital infrastructure platform.

By using Bitcoin to kill debt and partnering with real estate titans to build AI data centers, MARA is writing the playbook for how crypto-native companies can evolve into essential infrastructure players. The era of the pure-play, hold-forever miner is giving way to the era of the energy-arbitrageur—a company that mines Bitcoin when profitable, but builds the backbone of the AI economy when the opportunity arises.

For investors, the message is clear: the value proposition of MARA is no longer just about the price of Bitcoin. It is about the value of the power it controls and the balance sheet discipline it exercises to unlock it.

Discover more from The CoinStar

Subscribe to get the latest posts sent to your email.

On the morning of March 12, a message landed in OP Labs’ internal Slack channel that stopped engineers mid-keystroke. Jing Wang — co-founder of Optimism and CEO of OP Labs, the company building one of Ethereum’s most closely watched layer-2 networks — had informed 20 colleagues that their roles were being eliminated. The channel showed 102 members. The math was unsparing: roughly one in five had just been let go.

Wang shared the note publicly on X, framing the decision in unusually direct terms: “This decision reflects a narrowing of our focus, not our runway.” Crypto Times The full internal message went further. “This is not about finances. OP Labs is well capitalized with years of runway,” Wang wrote. “This is about doing fewer things well, making decisions faster, and reducing coordination overhead.” The Block

The statement was carefully constructed — almost preemptively defensive. And for good reason. The OP Labs layoffs didn’t emerge from a vacuum. They arrived barely three weeks after one of the most destabilizing events in Optimism’s history, in a market that has spent much of 2026 delivering hard lessons to crypto infrastructure builders who grew fat during the bull cycle.

The Shadow of Base’s Departure

To understand the strategic logic — and the underlying anxiety — behind this Optimism layer 2 job cut, you have to begin in February, when Coinbase’s Base network announced it was abandoning the OP Stack.

Base was the dominant chain in the Superchain ecosystem, accounting for approximately 70–96.5% of sequencer and gas fee revenue flowing to the Optimism Collective. BeInCrypto Its departure was not a minor partner reshuffling. It was the equivalent of a company losing its anchor client — the one whose logo appeared first on every investor deck, whose volume made every growth chart look credible.

Base’s exit triggered a 28% crash in the OP token to an all-time low of $0.12. Wang had said at the time: “This is a hit to near-term on-chain revenues.” Crypto Times As of mid-March, OP was trading at approximately $0.119 — down more than 55% year-to-date, with the all-time high of $4.84 set in March 2024 now a distant reference point. BeInCrypto

The official line from OP Labs is that the OP Labs restructuring is unrelated to Base’s exit. Technically, that may be defensible: the organization has disclosed significant treasury reserves and years of runway. But in practice, few strategic resets happen in isolation from the event that precedes them by three weeks. The loss of Base forced a reckoning about what the Superchain is actually for — and, by extension, how many people are needed to build it.

“Fewer Things, Done Exceptionally Well”

What makes Wang’s communication strategy notable is its framing. Rather than the standard corporate euphemisms — “rightsizing,” “organizational transformation” — she chose a phrase that reads almost like a product manifesto: do fewer things well.

To the remaining staff, Wang was explicit: “I want to be clear: We are not shuffling the same amount of work across fewer people. The goal is to do fewer things, and do them exceptionally well.” She added that she would follow up with clarity on what work continues and what stops — a signal that the restructuring involves cutting entire workstreams, not merely thinning headcount. Crypto Times

This is a meaningful distinction. A company that cuts staff while maintaining the same product surface area is in trouble. A company that cuts staff because it has genuinely decided to abandon certain initiatives is executing a strategy. Which one this is will become clear over the next two quarters.

For the Ethereum L2 scaling ecosystem, the answer matters enormously. Optimism’s Superchain concept — a shared infrastructure layer connecting multiple rollup chains — was the most ambitious attempt to create a federated layer-2 economy on Ethereum. Its viability now depends heavily on what OP Labs decides to stop doing.

The 2026 Roadmap: What Remains

Despite the turbulence, Optimism has set forth a clear roadmap for 2026, targeting faster block times, native interoperability, custom compliance controls to fit different regulatory environments, and zero-knowledge proof systems closely aligned with Ethereum’s quantum-proof ZK systems roadmap. The Block

Key strategic pillars that survive the restructuring:

- Native interoperability — the ability for chains within the Superchain to communicate without third-party bridges, a capability that remains genuinely differentiated in the L2 landscape

- ZK proof integration — aligning with Ethereum’s long-term roadmap toward provable computation, where Optimism’s current optimistic-fraud-proof model will eventually need to evolve

- OP Enterprise — a production-grade infrastructure product targeting fintechs and banks with 8-to-12-week deployment timelines, launched days before the layoffs Crypto Times

- Token buybacks — in January, OP token holders voted to approve a proposal directing 50% of Superchain revenue to monthly OP purchases The Block, signaling a shift toward value accrual for token holders

The enterprise infrastructure push is particularly telling. It suggests OP Labs is deliberately repositioning from a public-goods ethos — which defined its early culture and funding model — toward institutional revenue. That’s a significant cultural pivot, and one that may explain why certain roles no longer fit.

The L2 Competitive Landscape: A Darwinian Moment

The OP Labs layoffs 2026 arrive at a moment when Ethereum’s layer-2 ecosystem is undergoing its most intense competitive sorting to date. The narrative of endless expansion — more chains, more stack deployments, more developer grants — has collided with economic reality.

Arbitrum, which has spent 2026 aggressively courting institutional DeFi and gaming deployments, remains OP’s most direct competitor for developer mindshare. ZKSync and Starknet, both building on zero-knowledge architecture, have positioned themselves as the technically superior long-term bet. Coinbase’s Base, now pursuing its own unified stack, may emerge as a well-capitalized independent player. And newer entrants like Unichain — Uniswap’s dedicated L2 — and Sony’s Soneium have fragmented what was once a more predictable competitive landscape.

The crypto industry entered 2026 with a sharp hiring contraction. Data from crypto recruiting firms showed new job postings in January running at roughly 6.5 per day across major crypto job boards — down approximately 80% from the same period in 2025. Notable projects including Mantra, Polygon Labs, and Berachain all implemented workforce reductions in the opening weeks of the year. Crypto Times

Polygon Labs reportedly laid off roughly 60 employees in January. DL News The pattern is consistent: infrastructure builders that scaled headcount during the 2023–2024 bull cycle are now reconciling team size with the narrower, more defined work ahead.

The Severance Signal

One telling detail in the OP Labs announcement is the generosity of the exit packages. Severance starts at three months of base salary, with one additional month for each full year of service, capped at five months. All departing employees receive six months of continued health insurance and may retain their personal laptops. TechFlow

Wang also publicly vouched for departing employees, describing them as “talented engineers, operators, and builders” and inviting teams across the crypto ecosystem to reach out about hiring them. Crypto Times

This matters beyond optics. In a tight market where Ethereum’s builder community is relatively small and deeply interconnected, how a company treats departing employees in a downturn determines its ability to recruit in the next upturn. Wang’s approach — transparent communication, generous severance, personal referrals — is consistent with a leadership team that still expects to be competing for top engineering talent within 18 months.

Impact of OP Labs Restructuring on Ethereum Layer 2: A Measured Assessment

The instinct, in crypto markets, is to treat any staff cut as a harbinger of collapse. The OP token’s price reaction — sliding after the news broke — reflects that instinct. But the reality is more nuanced.

The bearish case: Base’s departure removed the largest single source of Superchain revenue. The remaining chain partners collectively represent a fraction of the economic activity that Base contributed. Without a major new chain joining the Superchain, the shared-revenue model that justified Optimism’s federated vision loses its most compelling proof point. The 2026 roadmap is ambitious, but ZK proof integration and native interoperability are multi-year technical programs, not near-term catalysts.

The bullish case: A leaner OP Labs, focused on enterprise infrastructure and a ZK-aligned technical roadmap, may actually be better positioned than the sprawling organization that tried to serve public-goods funding, developer tooling, chain deployment, governance, and protocol research simultaneously. Wang’s language — cutting workstreams, not just headcount — suggests genuine strategic prioritization rather than financial triage. And the enterprise infrastructure pivot, if successful, opens revenue streams that don’t depend on sequencer fees from Superchain partners.

The impact of OP Labs restructuring on Ethereum layer 2 more broadly may be limited. Ethereum scaling is not dependent on any single L2 team. But Optimism’s Superchain concept — if it survives and executes — represents a meaningful model for how rollup interoperability could work at scale. Its failure would not kill Ethereum scaling; it would simply mean that federated rollup coordination gets solved differently.

What the ZK Roadmap Means for Optimism’s Survival

The most strategically important element of OP Labs’ 2026 roadmap is its commitment to ZK proofs. Currently, Optimism uses an optimistic fraud-proof model: transactions are assumed valid unless challenged within a dispute window. ZK proofs, by contrast, provide cryptographic verification of every transaction — faster finality, stronger security guarantees, and eventual alignment with Ethereum’s own cryptographic trajectory.

The problem is that ZK proof systems are extraordinarily complex to build and audit, and the talent market for ZK engineers is among the tightest in all of software development. Cutting 20% of staff while simultaneously committing to ZK integration is a bet that the remaining team is sufficiently specialized — that the roles eliminated were in workstreams that don’t touch the ZK roadmap.

If that bet is correct, OP Labs emerges from this restructuring as a more technically focused, enterprise-ready organization with a credible path to ZK-verified rollup infrastructure. If it isn’t — if the departing engineers included people whose expertise was quietly essential to the ZK work — the next 18 months will be difficult.

A Narrowing of Focus, or a Narrowing of Ambition?

There is a version of this story in which OP Labs’ decision is exactly what Wang says it is: a disciplined strategic reset by a well-funded organization that grew too broad and is now sharpening its edge. The enterprise pivot, the ZK roadmap, the buyback program — these all point toward a more coherent theory of value than the original public-goods narrative, which, however admirable, struggled to translate into sustainable economics.

There is another version in which Base’s departure exposed a structural fragility in Optimism’s model that no amount of strategic repositioning can fully resolve — a version where the Superchain’s federated economics only ever made sense with a participant the size of Coinbase anchoring it.

For investors in OP, developers building on the stack, and the broader Ethereum ecosystem watching the Optimism Superchain update closely, the difference between these two versions will become legible over the next two quarters. Wang’s bet is on the first version. The market, for now, is pricing in something closer to the second.

What’s clear is that the era of infinite-expansion layer-2 infrastructure building — more teams, more chains, more workstreams — is over. What comes next will be built by leaner organizations making harder choices about where, precisely, they are irreplaceable. OP Labs has just announced, loudly, that it intends to find out whether it still is.

FAQs(FREQUENTLY ASKED QUESTIONS)

What exactly happened with OP Labs layoffs in 2026? OP Labs, the development company behind the Ethereum layer-2 network Optimism, cut 20 employees on March 12, 2026 — approximately 20% of its roughly 102-person team. CEO Jing Wang said the decision was driven by a desire to narrow strategic focus, not by financial pressure.

Why did OP Labs cut roles after Base’s departure? While OP Labs denied a direct connection, Base’s exit in February 2026 — which removed up to 96.5% of Superchain sequencer revenue — preceded the layoffs by three weeks. The restructuring appears to reflect a recalibration of operational scope following the loss of the Superchain’s anchor chain.

What is the Optimism Superchain and why does it matter? The Optimism Superchain is a shared infrastructure layer connecting multiple rollup chains on Ethereum. It allows chains built on the OP Stack to share sequencer infrastructure and revenue. Base was the largest participant before its departure.

Is OP Labs financially stable? According to CEO Jing Wang, yes. The company has “years of runway” and is “well capitalized.” Departing employees received severance of 3–5 months’ salary plus six months of healthcare benefits — packages that suggest financial health.

What is OP Labs’ plan for 2026? The 2026 roadmap includes faster block times, native rollup interoperability, ZK proof integration aligned with Ethereum’s quantum-proof roadmap, enterprise infrastructure products (OP Enterprise), and a token buyback program using 50% of Superchain revenue.

Discover more from The CoinStar

Subscribe to get the latest posts sent to your email.

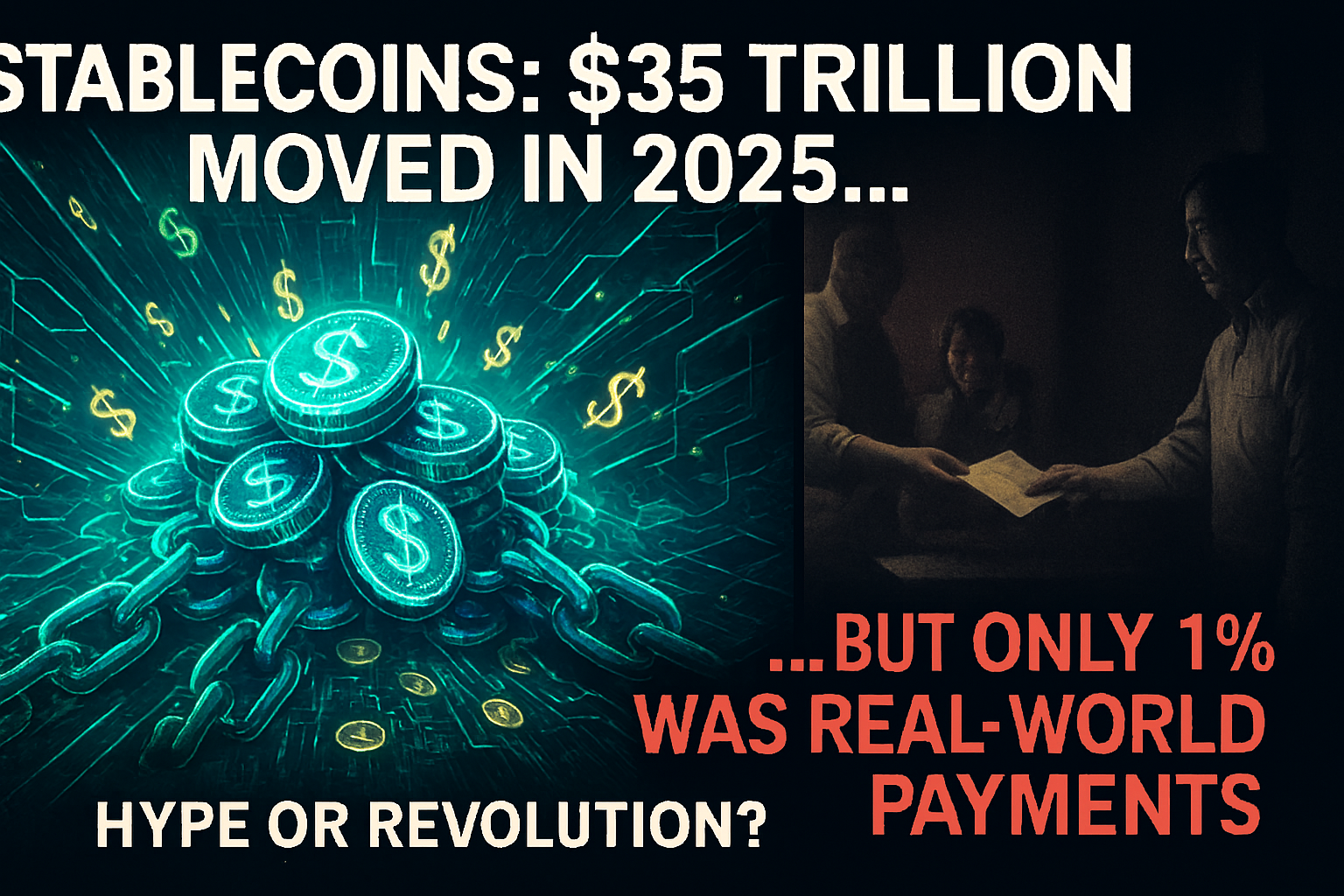

The numbers seem almost too staggering to believe: stablecoins processed approximately $35 trillion in transaction volume throughout 2025, a figure that dwarfs the annual GDP of most nations and rivals the combined output of the United States and China. Yet buried within this eye-popping headline lies a sobering reality that few mainstream outlets have properly examined—only about 1% of that colossal volume, roughly $380–390 billion, actually facilitated genuine real-world payments.

The remaining 99%? It’s a churning ocean of crypto trading, arbitrage, internal protocol transfers, and DeFi activity that never touches the “real economy” most of us inhabit. This isn’t merely a statistical footnote—it’s a fundamental tension that defines where stablecoins stand today and where they might head tomorrow.

The Illusion of Scale: Understanding What $35 Trillion Really Represents

When McKinsey and Artemis Analytics published their groundbreaking analysis examining 2025’s stablecoin transaction volume, they exposed something the cryptocurrency industry doesn’t often discuss candidly: raw on-chain volume tells an incomplete, even misleading story.

Think of it this way: if you withdraw $100 from an ATM, deposit it back into your account an hour later, then repeat this process ten times daily, you’ve generated $1,000 in “transaction volume” without actually purchasing anything. Stablecoins operate under similar dynamics, but at planetary scale.

The $35 trillion figure captures every movement of digital dollars like USDT, USDC, and their competitors across blockchain networks. This includes:

- Crypto exchange trading and liquidity provision: Traders using stablecoins as the “base currency” to buy Bitcoin, Ethereum, and thousands of altcoins

- Arbitrage operations: Sophisticated algorithms exploiting tiny price differences across exchanges, sometimes moving the same capital dozens of times per hour

- DeFi protocol interactions: Lending, borrowing, yield farming, and liquidity pool transactions that recirculate assets without ever converting to goods or services

- Internal custodial transfers: Exchanges and platforms shuffling assets between hot wallets, cold storage, and user accounts

As CoinDesk reported, this phenomenon isn’t unique to 2025, but the scale has grown exponentially. What matters for stablecoins real world payments adoption isn’t the headline number—it’s what happens when digital dollars leave the crypto ecosystem and enter the traditional economy.

Breaking Down the Real 1%: Where $390 Billion Actually Went

That $380–390 billion in genuine payments, while representing just a sliver of total volume, tells a far more interesting story. According to the McKinsey-Artemis breakdown, this real-world stablecoin transaction volume 2025 divided into several distinct categories:

Business-to-Business (B2B) Payments: $226 Billion

The largest segment involves companies using stablecoins for cross-border commercial transactions. A manufacturer in Vietnam receiving payment from a German distributor might prefer USDC settlement that arrives in minutes rather than waiting 3–5 days for traditional wire transfers that cost $25–50 in fees.

These transactions often involve:

- International trade finance

- Supply chain payments

- Corporate treasury management

- Cross-border invoice settlement

Remittances and Payroll: $90 Billion

Migrant workers sending money home have discovered stablecoins as an alternative to traditional remittance services that often charge 6–8% in fees. A construction worker in the UAE can now send USDT to family in the Philippines for pennies in transaction costs.

Similarly, global companies are experimenting with stablecoin-based payroll, particularly for remote contractors in emerging markets where accessing traditional banking infrastructure proves difficult or expensive.

Capital Markets Settlement: $8 Billion

Though still nascent, tokenized securities and institutional DeFi applications are beginning to use stablecoins for near-instantaneous settlement of trades that traditionally take T+2 days to clear.

Other Real-World Uses: $56–66 Billion

This catchall includes e-commerce purchases, bill payments, charitable donations, and various consumer transactions that convert stablecoins to fiat or goods and services.

Putting It in Perspective: The Vast Ocean of Global Payments

Here’s where the numbers become truly humbling. The global payments market processes over $2 quadrillion annually—that’s $2,000 trillion, or roughly 57 times larger than the total stablecoin on-chain volume and 5,100 times larger than stablecoins’ real-world payment contribution.

To put this in context: stablecoins currently represent approximately 0.02% of global payment flows. That’s two-hundredths of one percent.

Compare this to established players:

| Payment Network | Annual Volume (2025) | Market Share |

|---|---|---|

| Visa | ~$14 trillion | 0.7% of global payments |

| Mastercard | ~$9 trillion | 0.45% of global payments |

| SWIFT/Wire Transfers | ~$150 trillion | 7.5% of global payments |

| Stablecoins (Real Payments) | ~$390 billion | 0.02% of global payments |

The comparison reveals both the massive runway ahead and the enormous gap between current reality and crypto evangelists’ grander visions. As The Financial Times explored, stablecoins could theoretically shake up global payments—but “could” and “currently are” remain vastly different propositions.

Five Reasons Why Most Stablecoin Volume Isn’t “Real”

Understanding why 99% of stablecoin activity remains contained within crypto markets requires examining the structural dynamics of digital asset ecosystems:

1. Stablecoins Serve as Crypto’s Internal Plumbing

In traditional finance, the dollar functions as the reserve currency. In crypto markets, stablecoins play this role. When a trader wants to exit Bitcoin without converting to fiat, they sell for USDT or USDC. This creates enormous circular flows that inflate transaction counts without touching real-world commerce.

2. High-Frequency Trading Amplifies Apparent Activity

Algorithmic trading bots can execute hundreds of transactions per minute, moving between stablecoins and volatile assets. A single $1 million in capital might generate $50 million in daily volume through rapid-fire trades—yet this represents speculative positioning, not economic activity.

3. DeFi Protocols Require Constant Rebalancing

Automated market makers, lending protocols, and yield aggregators continuously move stablecoins between pools, strategies, and positions. These are legitimate financial operations but don’t represent new economic value creation or real-world payments.

4. Arbitrage Creates Volume Without Net Transfers

When USDC trades at $1.001 on one exchange and $0.999 on another, arbitrageurs pounce, moving millions to capture fractions of pennies. These transactions balance out crypto market inefficiencies but never exit the ecosystem.

5. Custodial Consolidation Inflates On-Chain Counts

Large exchanges periodically consolidate user funds from thousands of addresses into central treasuries, then redistribute them. Each movement registers as a transaction, multiplying the apparent volume.

The Regulatory Tailwind: How Policy Might Unlock Growth

Despite the current disparity between hype and stablecoin real economy adoption, 2026 has brought unprecedented regulatory clarity that could fundamentally shift these dynamics.

The GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins), passed in late 2025, established the first comprehensive federal framework for stablecoin issuers. Key provisions include:

- Reserve requirements: 1:1 backing with high-quality liquid assets

- Regular audits: Quarterly attestations by registered accounting firms

- Issuer licensing: Federal oversight for stablecoin providers

- Consumer protections: Redemption guarantees and disclosure requirements

As The Economist analyzed, this regulatory clarity removes a major barrier for institutional adoption. Banks and payment processors that previously avoided stablecoins due to legal uncertainty can now integrate them with defined compliance frameworks.

“Regulatory legitimacy is the bridge between crypto’s $35 trillion of internal volume and the $2 quadrillion real-world payment opportunity,” noted a recent McKinsey infrastructure report. The question isn’t whether institutions will adopt stablecoins, but how quickly traditional finance can integrate blockchain-based settlement rails.

Institutional Adoption: The Visa and Stripe Effect

The most consequential development in stablecoins vs traditional payments isn’t happening on crypto-native platforms—it’s occurring within legacy financial infrastructure.

Visa’s Stablecoin Settlement Network

In mid-2025, Visa announced it would enable merchants to receive settlement in USDC, initially for cross-border transactions. By year-end, over 8,000 merchants across 47 countries had activated this option. While Visa doesn’t disclose exact volumes, industry analysts estimate this accounted for roughly $12–15 billion of 2025’s real-world stablecoin payments.

The value proposition is straightforward: a coffee shop in Mexico City receiving payment from a tourist’s U.S. credit card can now get settled in USDC within hours rather than waiting days for traditional currency conversion and bank transfers. The shop then converts USDC to pesos through local exchanges at competitive rates.

Stripe’s USDC Payment Integration

Stripe’s decision to support USDC payments for its 4 million merchant partners potentially represents the largest single on-ramp for mainstream stablecoin payments growth. Early adoption has been modest—most customers still prefer traditional cards—but Stripe reported $8 billion in USDC payment processing throughout 2025.

The breakthrough moment may arrive when Stripe enables automatic stablecoin-to-fiat conversion at checkout, removing the cryptocurrency knowledge barrier. A customer paying with USDC wouldn’t need to understand blockchain technology any more than they need to understand ACH networks when paying with a bank account.

The Remittance Revolution That’s Actually Happening

While B2B payments grab headlines, stablecoin remittances payroll applications are delivering the most tangible human impact.

Traditional remittance services—Western Union, MoneyGram, and similar providers—charge average fees of 6.2% globally, according to World Bank data. For workers sending $200 home monthly, that’s $148.80 in annual fees, nearly a full month’s remittance lost to transaction costs.

Stablecoin alternatives charge $0.50–2 per transaction regardless of amount, representing 96–99% cost savings for many users. The $90 billion in remittances and payroll processed through stablecoins in 2025 likely saved senders approximately $5–6 billion compared to traditional channels.

Real-world adoption is concentrated in corridors where:

- Traditional banking infrastructure is weak or expensive

- Cryptocurrency literacy is growing

- Regulatory environments tolerate digital asset usage

- Local currency instability makes dollar-pegged assets attractive

Key corridors include U.S.-to-Mexico ($23B), UAE-to-Philippines ($14B), U.S.-to-Nigeria ($11B), and various Southeast Asian routes. These aren’t hypothetical use cases—millions of people are actively choosing stablecoins over legacy alternatives.

The Skeptic’s Case: Why 1% Might Be the Ceiling, Not the Floor

Balanced analysis demands examining why stablecoins real world payments might not dramatically expand beyond current levels. Several structural challenges complicate the bullish narrative:

Consumer Friction Remains High

Despite improved user interfaces, using stablecoins for everyday payments still requires:

- Setting up a digital wallet

- Understanding private key security

- Managing gas fees and network congestion

- Converting between crypto and fiat

- Tracking tax implications of each transaction

For most consumers in developed markets with efficient banking systems, this complexity offers little benefit. Venmo, Zelle, and instant bank transfers already provide fast, free, familiar payment experiences.

Merchant Adoption Lacks Incentive

Businesses operating on thin margins have little reason to adopt new payment rails that introduce operational complexity. Credit cards offer consumer protections and purchase financing that stablecoins don’t. The 2–3% merchant fee might be annoying, but it’s predictable and comes with dispute resolution.

Speculative Dominance Won’t Disappear

The crypto market’s fundamental nature—high volatility, 24/7 trading, global access—naturally generates enormous internal transaction volume. Even if real-world payment usage grows 10x, crypto trading activity might grow 20x, maintaining or even increasing the current disparity.

Regulatory Uncertainty Persists Globally

While the U.S. passed the GENIUS Act, China has banned crypto transactions entirely, the EU’s MiCA framework remains in implementation, and dozens of countries lack clear policies. A truly global payment network needs global regulatory harmonization—something that could take decades.

What 2026 and Beyond Might Bring

Despite these challenges, multiple credible forecasts project significant expansion. Various industry analyses suggest stablecoins could capture $2–4 trillion in real-world payment volume by 2030—roughly 5–10x current levels.

This growth would likely come from:

Institutional Adoption Cascades

As major banks, payment processors, and fintech companies integrate stablecoin rails, the network effects become self-reinforcing. When your bank, your employer, and your favorite retailers all accept USDC, the friction of adoption disappears.

Several major U.S. banks announced in late 2025 they would offer USDC custody and payment services in 2026, following regulatory approval. If Bank of America’s 68 million customers can send stablecoin payments as easily as Zelle transfers, adoption could accelerate dramatically.

Emerging Market Leapfrogging

Just as many developing nations skipped landline infrastructure and jumped directly to mobile phones, stablecoin adoption might surge in regions where traditional banking is weakest. When the choice is between a unreliable local bank charging high fees and a smartphone app offering instant dollar-denominated transfers, many will choose the latter.

Programmable Payment Innovation

Stablecoins enable payment capabilities impossible with traditional rails: automatic recurring payments, conditional escrow, instant cross-border settlement, and integration with smart contracts. As developers build applications leveraging these features, new use cases may emerge that drive organic adoption.

Tokenization of Real-World Assets

As securities, real estate, commodities, and other assets become tokenized, stablecoins serve as the natural settlement layer. A tokenized Treasury market alone could generate hundreds of billions in genuine stablecoin transaction volume.

The Measurement Problem: Separating Signal from Noise

One under-discussed issue is that as stablecoin adoption grows, distinguishing “real” from “speculative” volume becomes harder, not easier.

Consider a small business that accepts USDC payments, holds some reserves in stablecoin-denominated money market funds earning yield, and periodically rebalances between USDC and USDT based on liquidity needs. Are those rebalancing transactions “real world payments” or “crypto trading”?

As the line between DeFi and TradFi blurs—with institutional money market funds, tokenized securities, and blockchain-based trade finance—the very categories we use to evaluate stablecoin adoption may need rethinking.

Perhaps the more relevant question isn’t “What percentage is real-world payments?” but rather “How effectively are stablecoins serving as monetary infrastructure?” By that measure, even today’s 1% represents meaningful progress.

The Deeper Meaning: What This Really Tells Us

The $35 trillion versus $390 billion disparity isn’t a story of failure—it’s a snapshot of an immature financial technology finding its footing.

Every transformative payment innovation followed a similar pattern. Credit cards existed for decades serving primarily affluent consumers before becoming ubiquitous. PayPal spent years as a platform for eBay power sellers before becoming mainstream. Mobile payments were “always about to take off” for a decade before actually doing so.

The fact that 99% of stablecoin volume remains within crypto markets simply reflects where the technology currently finds its strongest product-market fit. Stablecoins solve real problems for crypto traders, DeFi users, and blockchain developers. They’re starting to solve real problems for remittance senders, cross-border businesses, and underbanked populations.

The trajectory matters more than the snapshot. If real-world stablecoin payments grow from $390 billion in 2025 to $600 billion in 2026, to $1 trillion in 2027, the percentage might still look insignificant—but the absolute impact would be transformative for millions of users.

A More Nuanced Future

The stablecoin narrative requires moving beyond binary thinking—beyond questions of whether they’ll “succeed” or “fail,” whether they’re “revolutionary” or “overhyped.”

The reality emerging from 2025’s data is that stablecoins have already succeeded at specific use cases: providing dollar liquidity in crypto markets, enabling efficient DeFi protocols, offering cost-effective remittances in certain corridors, and facilitating cross-border B2B payments for early adopters.

Whether they expand beyond these niches to challenge Visa, Mastercard, and traditional banking depends on factors still in flux: regulatory frameworks, institutional adoption pace, user experience improvements, and whether compelling consumer applications emerge.

The $35 trillion headline is impressive but misleading. The $390 billion reality is modest but meaningful. The gap between them represents both the challenge and the opportunity—a reminder that transforming global payments is measured in decades, not years, and that the distance between potential and practice remains vast.

For now, stablecoins are a powerful tool searching for mass-market purpose, having found genuine value in pockets of the global economy while still operating largely at the margins of mainstream finance. Whether that changes by 2030 may determine if we look back at 2025 as the beginning of a payment revolution or merely as another chapter in crypto’s long history of unfulfilled promises.

The most honest answer to “What does $35 trillion in stablecoin volume really mean?” might simply be: we’re still figuring it out—and that’s perfectly acceptable for a technology that’s barely a decade old attempting to reimagine infrastructure that took centuries to build.

Discover more from The CoinStar

Subscribe to get the latest posts sent to your email.

-

AI4 months ago

AI4 months agoThe Chatbot Era is Over: Why OpenAI’s Pivot to Hardware with Foxconn Changes Everything

-

AI5 months ago

AI5 months agoThe Top 10 Performing Crypto Coins in 2025: The Definitive Analyst Report on Price Potential, AI Integration, and Institutional Adoption

-

Aviation4 months ago

Aviation4 months agoAirbus A320 Recall: A Crisis of Confidence in Global Aviation

-

AI3 months ago

AI3 months agoBitcoin Poised For ‘Boring’ 2025 Close – Here’s When BTC’s Real Test Will Come

-

AI4 months ago

AI4 months agoHow AI-Driven Tokens Are Reshaping DeFi in 2025

-

News4 months ago

News4 months agoApple Pocket: The Most Controversial Tech Accessory

-

Acquisition4 months ago

Acquisition4 months agoDaily Mail Owner Strikes £500m Deal for Telegraph Amid Regulatory Scrutiny

-

Business4 months ago

Business4 months agoCloudflare Down: Twitter, ChatGPT, and Major Websites Hit by Global Internet Outage